Why to invest in Ukraine through Cyprus? Arthur A. Nitsevych

International law offices & Veritas Legal advisers Odessa - Kiev - Nikolaev - Ilyichevsk

March 2007 Why to invest in Ukraine through Cyprus?

Many clients ask me as a lawyer a direct question what jurisdiction is the best one to invest in Ukraine. Can you give us a feel for the percentage of investors into Ukraine that use Cyprus-based vehicles? Of course, every case is a unique one. But let’s see together. According to the official Ukrainian statistics, the growth of foreign direct investment in 2005 hit a record high of $7.328 bln, which is 4.7 times more than in 2004. As of 1 July 2006, according to the Ukrainian Statistics Committee, the largest share of FDI to Ukraine came from Germany ($5.503 bln or 29.9%), Cyprus ($2.042 bln or 11.1%), Austria ($1.506 bln or 8.2%), UK ($1.435 bln or 7.8%) and USA ($1.322 or 7.2%).

Looking at our long experience in international tax planning and Cyprus' numerous advantages we can declare Cyprus compares favourably with many other similar locations. What makes us believe so? Strategic geographic location, excellent commercial infrastructure, political stability, favourable tax incentives, high standard of living and European lifestyle have contributed towards its development as an important financial cent.

Though located in the often stormy Middle East area, Cyprus is a centre of democracy and stability where businessmen from all over the world may run their affairs in a harmonious and friendly environment. The rule of law is a well-protected principle.

Cyprus has one of the most strategic geographic locations in the world. The island is situated at the crossroads of Europe, Asia and Africa. In addition, the Island's time zone is convenient to all other regional centres and this is enhanced by its excellent telecommunication links. Cyprus is also within easy flying time of the rest of Europe and the Middle East. Above all visitors from more severe climates will enjoy the excellent weather conditions prevailing in Cyprus.

The policy of the authorities has been directed to assist and promote foreign participation in the island’s economy. But this has not in any way operated to affect their respectability or good standing in the eyes of the international business community. Indeed, the authorities managed to succeed in maintaining a balance.

The commercial infrastructure of Cyprus, well developed, lends itself ideally to all forms of business activities. In particular it helps with a civilized environment, pleasant working conditions, comfortable accommodation and comparatively low operational costs and living expenses. A wide range of professional services are offered, including law and accounting firms.

The English legal system, practice and procedures, which Cyprus acquired during the time it was a British colony, have continued after independence despite the subsequent promulgation of further legislation. Moreover, although the official languages of the Republic are Greek and Turkish, English is spoken by the majority of the population.

The Island's telecommunication system compares favourably with the highest international standards and direct dialing telephone connections are available to all world centres.

The Cypriot authorities are firmly committed to forging and maintaining strong bonds of friendship with all neighbouring states and with countries further abroad. In addition, the official policy is one of fostering and promoting good relations with all international organizations.

Cyprus is a member of numerous international associations, including the United Nations, the Council of Europe, the Commonwealth, and the Non-Aligned Movement.

So, now having got an understanding on the political and business background let’s have a look at the tax framework. New legislation has been effective from January 1st 2003 and regulates the tax treatment of Cyprus companies. The new legislation aims to conform to European Union law and the European Union code of conduct and abide by Cyprus' commitment to the Organization of Economic Cooperation and Development (OECD) to eliminate harmful tax practices.

The main features of the current tax system are the following:

• The taxable profit of all Cypriot companies is taxed at the rate of 10%. • Dividend income from abroad to Cyprus is wholly exempt from corporation tax provided the direct holding

is at least one per cent (1%) of the share capital of the overseas company. This exemption will not apply if the company paying the dividend engages in more than fifty per cent (50%) of its activities in producing investment income and the foreign tax burden on the income of the company paying the dividends is substantially lower than that in Cyprus.

• There is no withholding tax on the payment of dividends, interest and royalties from Cyprus to non-

• In order to conform to the European Union, the new tax legislation adopts the appropriate European Union

directive which enables reorganizations, mergers, acquisitions and amalgamations of companies without tax implications.

• Dividend income and profits from the sale of securities and shares are exempt from corporation tax. • With 2 exceptions, profits from a permanent establishment abroad are exempt from corporation tax. • The treaties for the avoidance of double taxation which Cyprus has signed remain in force. There are

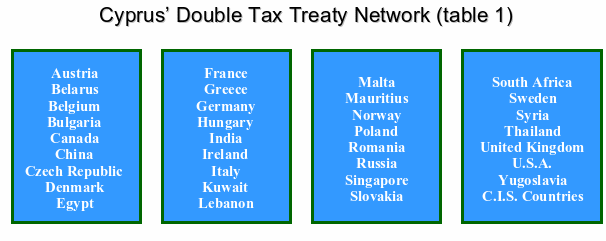

currently 34 such treaties (please, see the table 1). The existence of these treaties, combined with the low tax paid by a Cyprus company offer the possibilities for effective international tax planning as we will indicate in the examples below. The main objective of the double tax treaties is to avoid the double taxation of income earned in any of the two contracting countries. This is done through the tax sparing provisions whereby tax is credited against the tax that must be paid in the contracting state. The treaties also provide for reduced withholding taxes for dividends, interest and royalties.

The aim in Cyprus has always been to create not a tax haven but a tax incentive country. Therefore, regulations have always been adhered to. Permission from the Central Bank is necessary before a company can be established while at the end of each fiscal year audited accounts and annual returns must be submitted both to the Central Bank and to the tax authorities. Having said that, applications for the incorporation of a Cyprus company are processed efficiently by the Central Bank and the Registrar of Companies and the procedure can be completed in about a week. Local law firms and accountancy firms can provide nominee services for the administration of the company thus securing anonymity for the actual owner, where this is required. Instructions for the incorporation of a company can be given by fax or e-mail and the presence of the owner in Cyprus is not required.

With EU accession in May 2004 the status of a Cyprus holding company is enhanced further as it enjoys the reputation and privileges attached to a European company.

Foreign investors require from a holding company several things:

• The holding company must extract value from the operating company by way of dividends or gains

preferably free from withholding tax and capital gains tax, by means of a tax treaty or under the EU Parent/Subsidiary Directive and the domestic laws of the holding company jurisdiction must exempt such dividends and capital gains from local tax.

• It should be possible to take dividends out of the holding company without giving rise to any charge to tax

All these requirements are met in Cyprus, that’s why Cyprus is used as the location for the ultimate holding company and that’s why Cyprus is particularly suitable for investment vehicles with many countries.

What about the relations between Cyprus and Ukraine? If you have a look at the list of international documents protecting Cyprus investors in Ukraine I believe there will be no doubts:

• Convention on Settlement of investment disputes between states and foreign entities (effective as of

• Partnership and cooperation agreement between the EU and Ukraine (effective as of 01.03.1998), • Treaty between the Government of the USSR and the Government of the Republic of Cyprus of the

avoidance of double taxation with respect to taxes on income and estate (effective as of 26.08.83),

• Agreement between Ukraine and Cyprus on legal assistance in civil cases (effective as of 18.03.2006),

• Trade agreement between the Government of Ukraine and the Government of Cyprus (effective as of

Cyprus has always been one of the main sources of investments into Ukraine. Generally the advantages may be distributed into several groups:

• protection of assets, • tax optimization, • tax free gains on disposal.

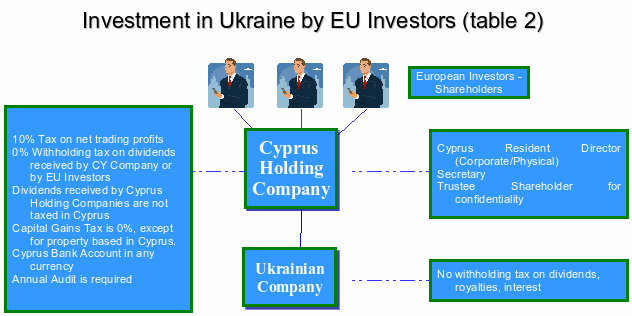

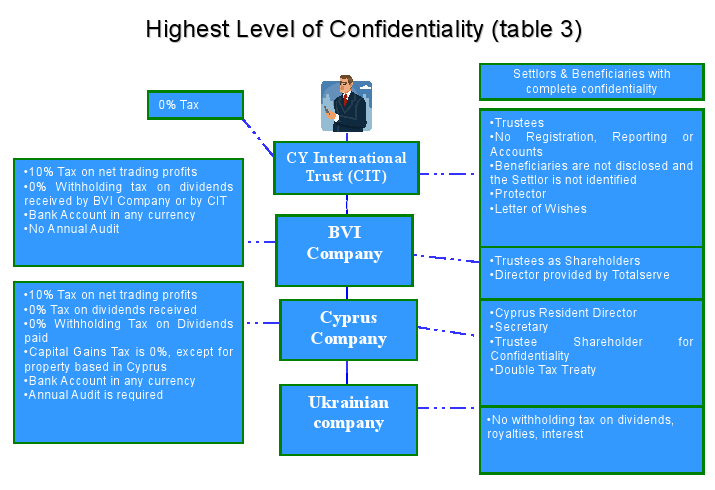

To be vivid we can illustrate the table 2 and 3. The highest level of confidentiality is provided with the use of another offshore structure. Royalties, dividends and interest paid from Ukraine to Cyprus are not taxed at all. Mergers and acquisitions may be carried out without taxes.

All the foregoing reasons make Cyprus a highly attractive jurisdiction for investment into Ukraine. Of course, every scheme is personal, so one must be careful building up his own business affairs and would better ask assistance from a professional in the sphere of tax planning.

The Author

Arthur A. Nitsevych, attorney-at-focused on shipping and commercial law mostly.

Born in 1971. He was educated at the Odessa State University as a philologist (English language and literature). Then he continued his education at the Odessa State Legal Academy. He also graduated from the Interregional Academy of Personnel Management in Kyiv and subsequently obtained a Degree of Master of science in accounting. He has got 10 years of practical experience. Fluent in English and Spainish. His areas of practice include investment legislation and settlement of tax disputes, maritime law.

International law offices & Veritas Legal advisers

Detection of Infectious Outbreaks in Hospitals through Incremental Clustering Timothy Langford1, Christophe Giraud-Carrier1, and John Magee21 Department of Computer Science, University of Bristol, Bristol, UK2 Department of Medicine, Microbiology and Public Health Laboratory, Cardiff, UK Abstract. This paper highlights the shortcomings of current systems of noso- comial infection control

HAIR TRANSPLANTING IN WOMEN Walter Unger Female Pattern Hair Loss (FPHL) is far more common than is generally recognized by physicians—including many dermatologists. There are three recognized general patterns of FPHL: A caudal and centrifugal pattern described by Ludwig in which hair in the hairline is maintained, though it may thin to varying degrees. In Venning’s and Dawber’s stu

• The holding company must extract value from the operating company by way of dividends or gains

preferably free from withholding tax and capital gains tax, by means of a tax treaty or under the EU Parent/Subsidiary Directive and the domestic laws of the holding company jurisdiction must exempt such dividends and capital gains from local tax.

• It should be possible to take dividends out of the holding company without giving rise to any charge to tax

All these requirements are met in Cyprus, that’s why Cyprus is used as the location for the ultimate holding company and that’s why Cyprus is particularly suitable for investment vehicles with many countries.

What about the relations between Cyprus and Ukraine? If you have a look at the list of international documents protecting Cyprus investors in Ukraine I believe there will be no doubts:

• Convention on Settlement of investment disputes between states and foreign entities (effective as of

• Partnership and cooperation agreement between the EU and Ukraine (effective as of 01.03.1998), • Treaty between the Government of the USSR and the Government of the Republic of Cyprus of the

avoidance of double taxation with respect to taxes on income and estate (effective as of 26.08.83),

• Agreement between Ukraine and Cyprus on legal assistance in civil cases (effective as of 18.03.2006),

• Trade agreement between the Government of Ukraine and the Government of Cyprus (effective as of

Cyprus has always been one of the main sources of investments into Ukraine. Generally the advantages may be distributed into several groups:

• protection of assets, • tax optimization, • tax free gains on disposal.

To be vivid we can illustrate the table 2 and 3. The highest level of confidentiality is provided with the use of another offshore structure. Royalties, dividends and interest paid from Ukraine to Cyprus are not taxed at all. Mergers and acquisitions may be carried out without taxes.

• The holding company must extract value from the operating company by way of dividends or gains

preferably free from withholding tax and capital gains tax, by means of a tax treaty or under the EU Parent/Subsidiary Directive and the domestic laws of the holding company jurisdiction must exempt such dividends and capital gains from local tax.

• It should be possible to take dividends out of the holding company without giving rise to any charge to tax

All these requirements are met in Cyprus, that’s why Cyprus is used as the location for the ultimate holding company and that’s why Cyprus is particularly suitable for investment vehicles with many countries.

What about the relations between Cyprus and Ukraine? If you have a look at the list of international documents protecting Cyprus investors in Ukraine I believe there will be no doubts:

• Convention on Settlement of investment disputes between states and foreign entities (effective as of

• Partnership and cooperation agreement between the EU and Ukraine (effective as of 01.03.1998), • Treaty between the Government of the USSR and the Government of the Republic of Cyprus of the

avoidance of double taxation with respect to taxes on income and estate (effective as of 26.08.83),

• Agreement between Ukraine and Cyprus on legal assistance in civil cases (effective as of 18.03.2006),

• Trade agreement between the Government of Ukraine and the Government of Cyprus (effective as of

Cyprus has always been one of the main sources of investments into Ukraine. Generally the advantages may be distributed into several groups:

• protection of assets, • tax optimization, • tax free gains on disposal.

To be vivid we can illustrate the table 2 and 3. The highest level of confidentiality is provided with the use of another offshore structure. Royalties, dividends and interest paid from Ukraine to Cyprus are not taxed at all. Mergers and acquisitions may be carried out without taxes.

All the foregoing reasons make Cyprus a highly attractive jurisdiction for investment into Ukraine. Of course, every scheme is personal, so one must be careful building up his own business affairs and would better ask assistance from a professional in the sphere of tax planning.

The Author

All the foregoing reasons make Cyprus a highly attractive jurisdiction for investment into Ukraine. Of course, every scheme is personal, so one must be careful building up his own business affairs and would better ask assistance from a professional in the sphere of tax planning.

The Author  Born in 1971. He was educated at the Odessa State University as a philologist (English language and literature). Then he continued his education at the Odessa State Legal Academy. He also graduated from the Interregional Academy of Personnel Management in Kyiv and subsequently obtained a Degree of Master of science in accounting. He has got 10 years of practical experience. Fluent in English and Spainish. His areas of practice include investment legislation and settlement of tax disputes, maritime law.

International law offices & Veritas Legal advisers

Born in 1971. He was educated at the Odessa State University as a philologist (English language and literature). Then he continued his education at the Odessa State Legal Academy. He also graduated from the Interregional Academy of Personnel Management in Kyiv and subsequently obtained a Degree of Master of science in accounting. He has got 10 years of practical experience. Fluent in English and Spainish. His areas of practice include investment legislation and settlement of tax disputes, maritime law.

International law offices & Veritas Legal advisers